Role

Structured Credit Trader

Specialization

ABS Consumer Loans

Location

New York, NY

FINRA

Series 7 · 63 · SIE

Dennis Kyalo

Structured Credit Trader

ABS Consumer Loans · Whole Loan Trading · Structured Products

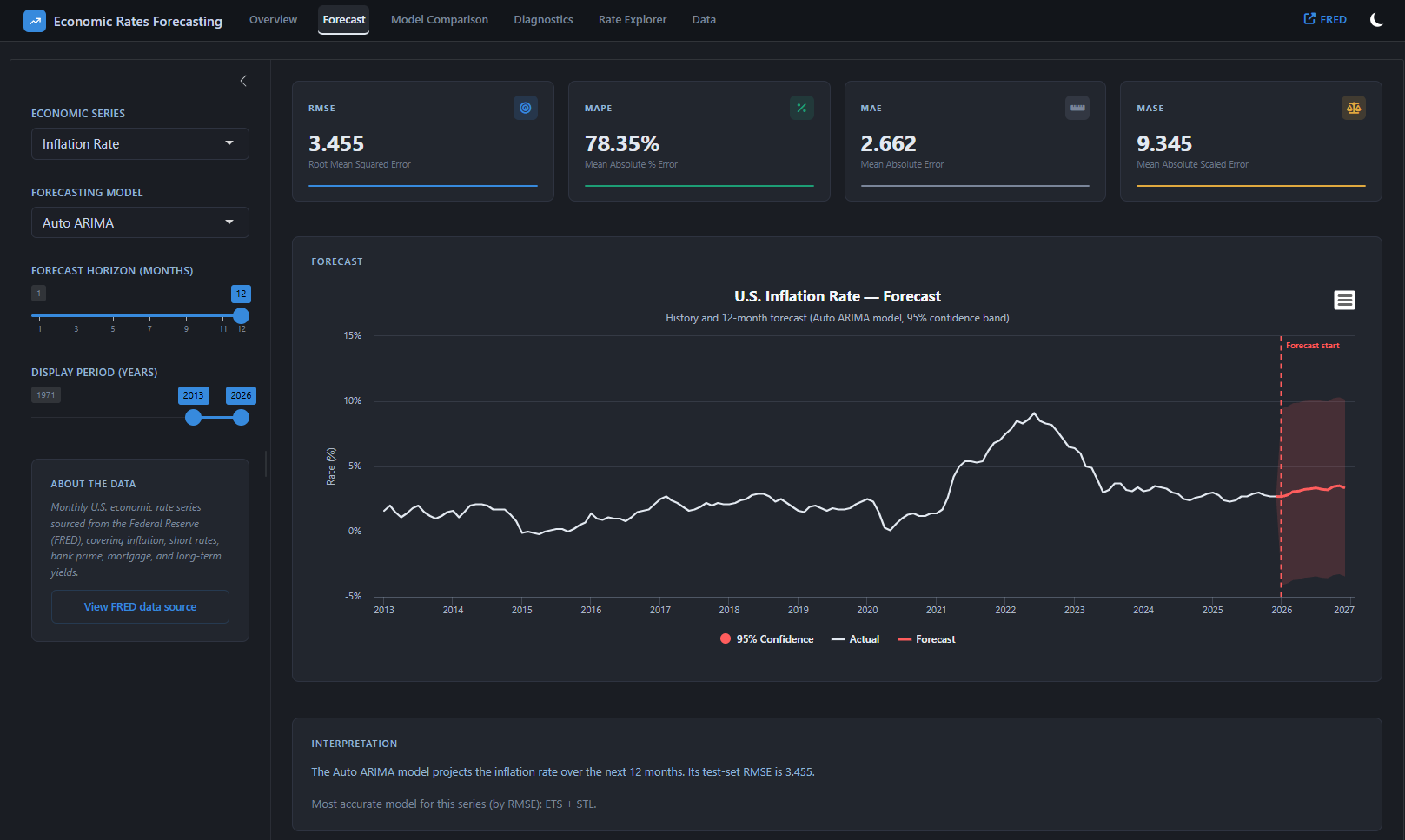

I specialize in ABS Consumer Loan Trading, focusing on the analysis, pricing, and trading of consumer loan portfolios. I leverage loan-level analytics, collateral surveillance, cash flow modeling, and credit performance analysis to evaluate investment opportunities and support structured credit trading decisions.

Beyond the trading desk, I am passionate about building AI-powered tools that make financial analysis faster, clearer, and more actionable.